What is APR, and Why Does it Matter?

We've put together this quick guide to APR to help you find out more about what it means and why you should care about it.

.jpg)

If you're looking for a credit card, mortgage or loan, you'll have seen the term APR. But do you know what it means or why it matters when you're looking for credit? We've put together this quick guide to APR to help you find out more about what it means and why you should pay attention to it.

What is APR, and Why Does it Matter?

So what does APR mean? It stands for Annual Percentage Rate and is essentially a quick and easy way to find out how much a loan will cost you. Whether you're taking out a mortgage, credit card or a personal loan, the APR shows you how much interest you'll pay and is calculated as an annual figure.

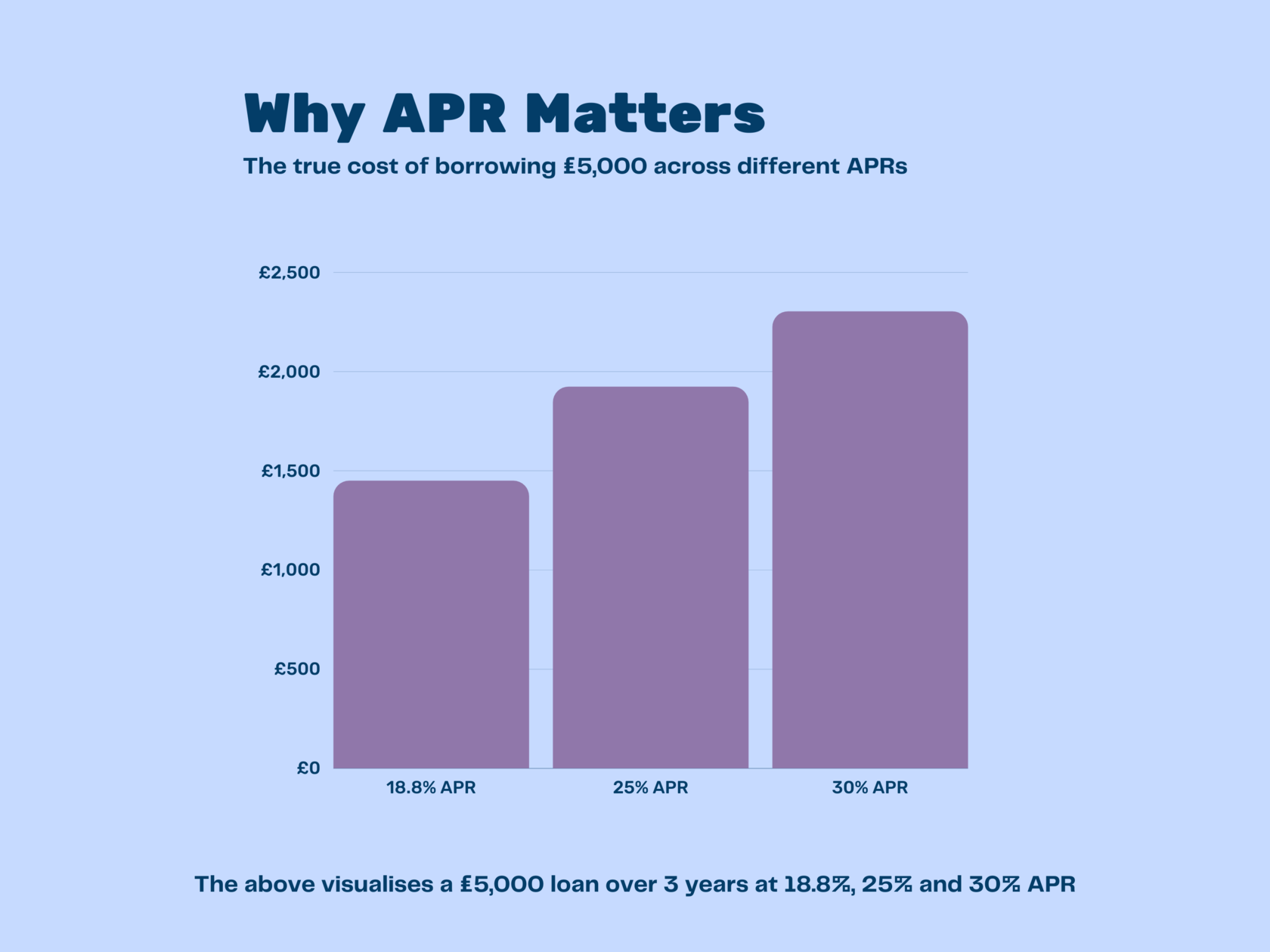

Let's take a look at a quick example. Joanne wants to take out a £5,000 loan and would like to spread the cost out over 3 years.

She goes to a comparison site to search for a loan and gets quotes from 3 different lenders. Here's what she sees:

What you can see above is that seemingly small differences in APR can make a big difference over time.

What are the different types of APR?

It's also important to know what type of APR applies to your credit.

- Introductory APR Lenders will often offer you a low initial rate. But beware, this will only apply for a limited amount of time. For example, you might be offered a 0% APR for six months. However, you'll pay a different rate after the introductory offer. When applying for a mortgage a 2 year introductory offer may sound great but remember mortgages are usually taken out for 25-30 years so you'll likely be paying a different rate for at least a couple of decades.

- Representative APR This is an advertised rate that at least 51% of people accepted for a loan will get. But that still means that nearly half the people who apply will have to pay a higher rate. Representative APR is a helpful comparison tool, but it may not be the rate you pay.

- Personal APR This is the crucial rate because it's the one you'll end up paying. Depending on your eligibility, this could be the same as the Representative rate or higher. The APR you'll be offered will depend on several factors such as your income, credit history and other personal financial information.

- Fixed APR A fixed APR rate won't change over the life of the loan, so you can easily budget for your monthly repayments.

- Variable APR Variable APR will track the base rate from the Bank of England. As the base rate moves up or down, so will your payments. Credit cards tend to use variable APR.

APR vs Interest Rate

When you're taking out a loan, you'll find out that interest rates and APR are two very different things. So what is the APR rate compared to the interest rate?

APR is a better representation of the total cost of your loan as it takes into account the total cost of borrowing, including any additional charges or fees a lender may charge. These could include set-up fees, ongoing service charges and early repayment fees. However, all lenders calculate APR the same way, using a formula set out in the Consumer Credit Act (1974).

Interest rates refer to the cost of borrowing an amount of money and is shown as a percentage of the total amount of your loan.

Because the APR includes these extra charges, it's a better thing to compare when weighing up different credit options.

How does APR work?

When you compare APR on different loans, you're looking for a figure that works for you. But the rate you pay can vary wildly depending on a range of factors, including your credit score. Many traditional lenders make decisions based solely on your credit score whereas others, like Abound, look at your entire financial situation.

But no matter what APR you're offered, you'll only pay it when you're in debt. So if you have a loan or credit card, the quicker you can pay it back, the less APR you'll pay.

Because APR includes additional fees, it's a great way to compare different loans. So a 17.5% APR loan will be more expensive than a 12.5% loan, although you should always check the small print for hidden charges.

It's worth being aware that APR only includes compulsory charges. Additional fees like payment protection or late payment charges will make your loan more expensive.

What factors affect your APR?

If you've borrowed money before and paid it back on time without missing any payments, you could be offered a great rate of APR. But if you've missed payments and exceeded your credit limit, then you'll be seen as a greater risk and pay more in APR.

All lenders look at several factors before they decide on your personal APR, including:

- Salary

- Credit score

- Expenditure

- Household income

- The amount you want to borrow

- The length of time you want to repay

As a general rule, when applying for a personal loan, the more you want to borrow and the longer the repayment term, the lower your APR. But don't be tempted by a lower rate to borrow more than you can repay.

What is a reasonable rate of APR?

The lower the APR, the less you'll pay overall in interest and charges. But you should always read the terms and conditions before you commit and check when a low rate introductory offer ends. For example, suppose you get a 0% credit card. You should always try and pay off any borrowing before the 0% period finishes.

It's always a good idea to shop around before you take out a loan or credit card. Most lenders will give you some idea of whether or not you're likely to be accepted by running an eligibility check. Also, look for lenders that run 'soft' eligibility checks, as these won't impact your credit scores.

How can Abound help?

At Abound we offer affordable loans based on the full picture, not just your credit score. You can apply for a Abound loan by clicking this link.

.jpg)

.jpg)

Fintern Limited, trading as Abound

3rd Floor

86-90 Paul Street

London, EC2A 4NE

United Kingdom

Abound is a trading name of Fintern Limited

Fintern Limited is registered in England & Wales No. 12472034

Spread a Smile is a registered charity No. 1152205

Fintern Limited, trading as Abound, is authorised and regulated by the Financial Conduct Authority, Firm Reference Number 929244

Fintern Limited is a member of Cifas – the UK's leading anti-fraud association, and we are registered with the Information Commissioner's Office in compliance with the Data Protection (Charges and Information) Regulations 2018 under registration ZA747930. See our Privacy notice for further details of how we use customers' data.